“To get through the hardest journey we need take only one step at a time, but we must keep on stepping.”

— Chinese Proverb

PEOPLE ARE BUUYING HOMES AND GETTING MORTGAGES!

Many believe that very few houses are selling and that almost no one can get a mortgage. We want to let everyone know that neither of these assumptions is true. Recently, the National Association of Realtors (NAR) released their Existing Homes Sales Report. According to the report there are, on average, 12,109 homes selling in the United States EACH and EVERY DAY! That means that approximately 12,000 houses sold yesterday, approximately 12,000 will sell today and approximately 12,000 will sell tomorrow. So the thinking that homes aren’t selling just isn’t true.

Another interesting fact in the report was that 72% of these transactions were accompanied by a mortgage. That means that approximately 8,719 people qualify for a mortgage on a daily basis in this country.

There are over 12,000 homes sold and over 8,000 mortgages granted every day. The real estate market is doing better than many believe.

FANNIE EXTENDS MORTGAGE RELIEF TO UNEMPLOYED

Fannie Mae says it will be providing more mortgage aid to the unemployed, possibly extending the forbearance period to up to a year to those who qualify.

Starting on March 1, Fannie Mae will require mortgage servicers to extend the forbearance relief to qualified unemployed borrowers for six months — without any approval needed from Fannie Mae. The government-sponsored enterprise also says special consideration will be made for some borrowers in suspending mortgage payments or reducing them for up to a 12-month period.

Fannie’s announcement follows on the heels of Freddie Mac’s announcement earlier this week about similar changes to its mortgage relief program for the unemployed. Freddie Mac announced it will begin offering a 12-month forbearance period to qualified unemployed borrowers starting on Feb. 1.

To qualify, mortgage servicers will determine if the “borrower has less than 12 months worth of mortgage payments in reserves and has monthly housing expenses above 31 percent of their incomes before extending a forbearance plan,” HousingWire reports.

During the third quarter of 2011, the GSEs issued more than 7,000 forbearance plans, according to the Federal Housing Finance Agency.

CREATING WEALTH THROUGH HOMEOWNERSHIP – THE PROOF

Several real estate economists have shown that the average homeowner accumulates more overall wealth than the average renter.[i] However, it is not clear how this is done. Is it that owned property usually appreciates at such a rate that, after considering leverage, returns to ownership are extraordinarily high? Said another way, might homeowners accumulate more overall wealth because ownership is a great levered equity creator through property appreciation? Or, is it that owners acquire greater wealth, on average, because they are systematically paying down a mortgage thereby creating equity thanks to loan amortization? In other words, paying off property creates wealth.

In ongoing research being conducted by Beracha and Johnson,[ii] these and other questions concerning homeownership and the accumulation of wealth are being investigated. In earlier research, Beracha and Johnson show that renting is the superior investment strategy; however, in this earlier strict horserace between buying and renting, a very bold assumption is made. Specifically, it is assumed that any rent savings (from lower rent versus mortgage payments) are reinvested without fail. Thereby, after balancing all of the costs and benefits from ownership and comparing them to renters’ portfolios from reinvesting rent savings, renting wins.

The question, however, very quickly becomes that, in a setting where Americans generally save less than 5% of their disposable income, is this assumption realistic and how might the removal of this reinvestment decision alter the outcome of the horserace between buying and renting? As part of their current research, this question is directly addressed. In particular, Beracha and Johnson find that after allowing renters to spend any rent savings on consumption (beer, cookies, healthcare, education, etc.), ownership leads to greater wealth accumulation, on average. The graph below highlights this finding.

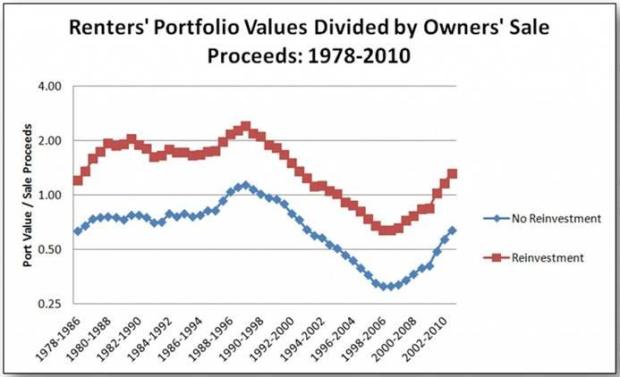

The graph looks at the ratio of renters’ portfolio values to owners’ proceeds from sale for the entire U.S. between 1978 and 2010 both with strict reinvestment of rent savings and without reinvestment of rent savings.[iii] Clearly, numbers greater than 1 indicate that renting leads to greater wealth accumulations, while numbers less than 1 indicate that homeownership creates greater wealth, on average.

When renters are forced to reinvest (top line in the graph), the results confirm the earlier findings of Beracha and Johnson (2012). That is, in a strict horserace between buying and renting, renting wins in the vast majority of cases. However, when renters are allowed to spend rent savings on consumption (i.e. economically act like the typical American consumer), homeownership wins in virtually all instances. Notice that in the bottom line of the graph (no reinvestment), the renters’ portfolio values divided by owners’ sale proceeds is great than 1 for only four of the 32 years of the study. Thus, when renters are allowed to spend rent savings, homeownership is the clear winner in the wealth accumulation horserace.

Finally, in the same current research, Beracha and Johnson find that allowing for property appreciation rates to increase as much as 20% over their actual historic values results in virtually no change in the outcomes concerning wealth accumulation. That is, property appreciation contributes only marginally to wealth accumulation.

Implications

Without proof many have speculated about this outcome for years. However, there is now actual quantifiable evidence that homeownership is not the great levered equity creator that it has so often been touted to be. Instead, it appears that homeownership creates extra wealth mainly through its ability to force owners to save rather than through property appreciation. Thus, homeownership appears to be a self-imposed savings plan, which through time leads to greater wealth accumulation as compared to comparable renters. In short, buying a home makes Americans save.

Who says that Americans are horrible savers? Apparently, we are not. We have simply been saving through our homes rather than putting our savings in the bank.

________________________________________

Endnotes

[i] Homeownership is the most viable path to wealth creation for the majority of Americans. See Engelhardt (1994), Haurin, Hendershott and Wachter (1996), and Rohe, Van Zandt and McCarhty (2002), among others.

[ii] Eli Beracha and Ken H. Johnson, 2012, Beer and Cookies Impact on Homeowners’ Wealth Accumulation, ongoing research.

[iii] The research assumes 8-year holding periods. When the holding period is allowed to vary between four and twelve years, the results change only marginally. Thus, holding period has very little to do with the results.

OPTIMISM BUILDS IN HOUSING MARKET

Several recent indicators for the real estate industry are pointing to a market that is on the mend and entering recovery mode.

Housing experts’ predictions for the new year tend to center around a market stabilizing before entering a gradual, albeit very slow, recovery. However, the tone is more upbeat than it has been in years for the housing market.

Here are a few of the signs that are showing the market moving in a more positive direction:

Home sales: Existing home sales are expected to increase 12 percent this year, following a 2 percent jump last year, Moody’s Analytics predicts. The signs are already showing: In November, pending home sales — a gauge for future home buying — reached its highest level in 19 months, the National Association of REALTORS® reported.

New-home market: Coming off of what could be considered the worst year for new-home building ever recorded, the sector is expected to bounce back this year. New-home sales and starts were already showing a rebound in the last few months of 2011. Moody’s is predicting that single-family housing starts will increase 37 percent this year, and new-home sales will soar 74 percent.

Housing stocks: Investors are starting to get optimistic about the possibility of a rebound too, and are turning to home builder stocks. These equities have recently outperformed the broader stock market and the S&P 1500 homebuilding index has increased 38 percent since mid-October, USA Today reports.

Consumer confidence: With mortgage rates at record lows and housing affordability high, about 71 percent of Americans say now is a good time to purchase a home. Also, more Americans are optimistic that home prices will rise over the next year — about 26 percent say prices will rise in 2012, an increase of 4 percent over the last survey, according to Fannie Mae’s December National Housing Survey

HOUSING NEWS: 11 TRENDS FROM 2011

The National Association of Realtors surveys homebuyers and sellers each year to uncover housing trends and monitor changes taking place in the industry. This year’s report highlights a number of trends that haven’t been seen in years. Here are just 11 highlights from the 2011 report.

1. In 2011, 37% of homebuyers were first-time buyers – which was down from 50% in 2010.

2. Last ye ar, 88% of homebuyers used the Internet to search for a home. That number was down slightly from a high of 90% in 2009.

3. The typical homebuyer searched for 12 weeks and viewed 12 homes.

4. The number of buyers who purchased their home through a real estate agent or broker climbed to 89% – a share that has steadily increased from 69% in 2001.

5. Nearly 1 out of 4 buyers said the application and approval process was “somewhat more difficult” than expectedand 16% reported it was “much more difficult” than expected.

6. About half of home sellers traded up to a larger and more expensive homeand 60% traded up to a new home.

7. The top 3 factors influencing neighborhood choice were: the quality of the neighborhood, the convenience to job, and the overall affordability of homes.

8. The typical seller lived in their home for 9 years. That n umber has increased from 6 years in 2007.

9. Although 61% of sellers said they reduced their asking price at least once, the average home sold for 95% of the listing price.

10. Only 10% of sellers sold their homes without the assistance of a real estate agent. Of those people, 40% knew the buyer prior to the sale.

11. The typical “for sale by owner” home sold for $150,000 compared to $215,000 for the average agent-assisted home sale.